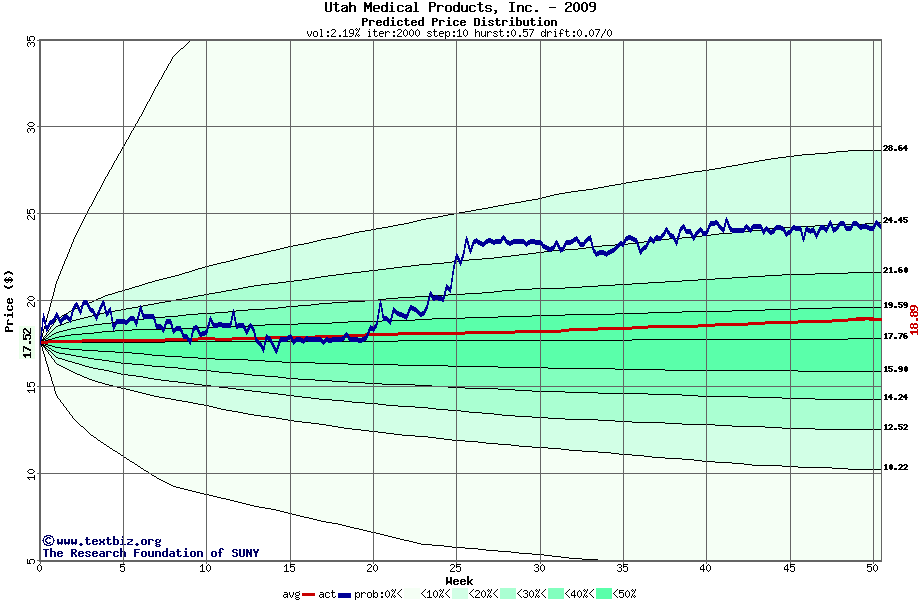

The following graph plots the year-to-date performance of the stock for 2009 compared to the probability calculated by a random walk model.

Initial Value*: $17.5

Hist. Volatility: 2.19%

Annual Drift: 7%

Final Value*: $24.3

Percentile: 79%

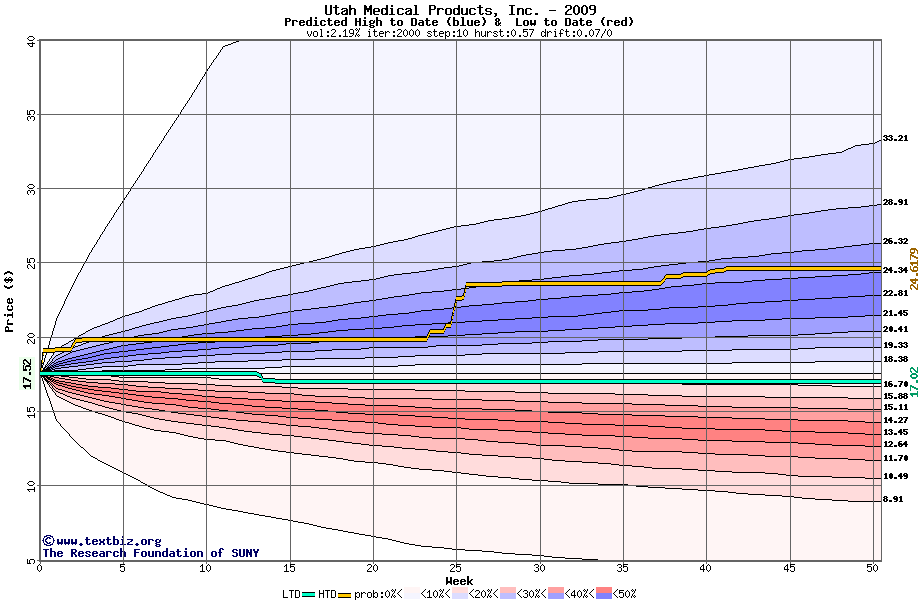

The high to date and low to date prices of the stock plotted against a random walk model for 2009 (what's this?).

© 2005, 2016, The Research Foundation of State University of New York, http://www.textbiz.org